Here’s a comprehensive guide about deciding when to outsource debt collection, combining the best insights and strategies for businesses:

Understanding the Need for Debt Collection Services

- Delinquent accounts: When customers fail to pay on time, it creates delinquent accounts that disrupt cash flow and impact your bottom line.

- Internal resource constraints: Chasing payments can be time-consuming for your in-house staff, diverting them from other essential duties.

- Specialized expertise: Debt collection agencies have specialized skills in negotiation, legal compliance, and skip tracing (finding debtors who have moved).

Signs It’s Time to Outsource Debt Collection

- Aging Accounts Receivable: If your accounts receivable are getting older (e.g., over 60 or 90 days), the likelihood of collecting them decreases. Outsourcing can improve recovery rates.

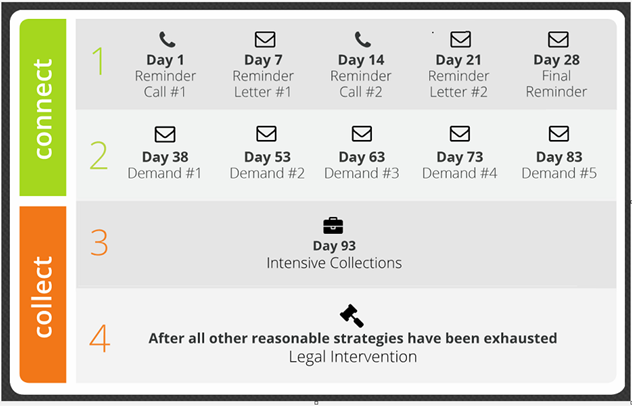

- Broken Promises: Clients who repeatedly break promises to pay are likely to continue doing so. A debt collection agency sends a clear message of seriousness about payment.

- High Volume of Delinquent Accounts: If your business has a significant number of unpaid invoices, outsourcing can provide the dedicated resources to effectively manage the process.

- Lack of Internal Resources: Smaller businesses may not have the time or staff to focus on persistent debt collection efforts. Third-party agencies free up your team to focus on core business activities.

- Avoidance of Contact: Debtors who ignore your calls and emails are often best addressed by the persistence and strategies used by collection agencies.

- Need for Specialized Skills: When complex negotiation, legal knowledge, or skip-tracing is required, collection agencies have the expertise and resources to handle it.

Factors to Consider When Choosing a Debt Collection Agency

- Fee Structure: Understand if they charge a flat fee, a percentage of collected debt, or a contingency fee (paid only if they successfully collect).

- Success Rate: Inquire about their success rates and compare them to industry averages.

- Reputation: Choose an agency with a strong reputation for ethical collections practices and compliance with the Fair Debt Collection Practices Act (FDCPA).

- Industry Specialization: Some agencies specialize in particular industries, such as healthcare or B2B. Consider this for optimal results.

- Communication and Reporting: Ensure they provide clear reporting and communication, keeping you informed throughout the process.

Advantages of Outsourcing Debt Collection

- Improved Cash Flow: Outsourcing leads to faster recovery of debts, improving your cash flow position.

- Freed-Up Resources: Your internal team can focus on revenue-generating activities rather than debt collection.

- Expertise and Efficiency: Specialized debt collection agencies have the resources and skills to maximize recovery rates.

- Legal Compliance: Reputable agencies ensure adherence to legal regulations, reducing your liability risks.

- Preserving Customer Relationships: Professional collection agencies can often maintain positive customer relationships while pursuing outstanding balances.

Cautions

- Potential Damage to Brand Reputation: It’s essential to select an agency committed to ethical and respectful debt collection.

- Loss of Control: You may have less direct control over the process compared to internal collection efforts.

- Costs: Factor in fees, and ensure the potential benefits outweigh the costs of outsourcing.

In Conclusion

Outsourcing debt collection can be the right solution for businesses facing challenges with overdue payments. If you’re seeing the signs of strained resources, uncollected debt, and broken payment promises, consider partnering with a reputable debt collection agency.